WASDE May 2026: Wheat Shock Confirmed, Soybean Oil Demand Surges, Corn Tightens

The USDA’s first full 2026/27 outlook delivered one of the most important agricultural commodity reports of the year so far. Wheat shifted sharply bullish, soybean oil received a major biofuel-driven demand boost, and global corn stocks moved toward historically tight levels.

Wheat

U.S. production falls sharply, ending stocks tighten, and global output drops from last year’s record.

Corn

U.S. stocks fall and global ending stocks are projected near the lowest level since 2013/14.

Soybeans

Larger production is partly offset by stronger crush and higher exports.

Soybean Oil

Biofuel use jumps sharply, pushing projected prices higher.

Sugar

Lower U.S. production and a tighter stocks-to-use ratio support the market.

Cotton

Production is lower, but the market still lacks the same tightness seen in wheat or soybean oil.

The March warning: wheat was already on the radar

One of the most interesting aspects of this report is that the wheat story did not appear out of nowhere. After the USDA Prospective Plantings report at the end of March, we already highlighted that wheat could become a key market to watch in 2026.

The May WASDE now confirms this risk. What looked like a potential issue in March has turned into one of the most important bullish shifts in the agricultural complex.

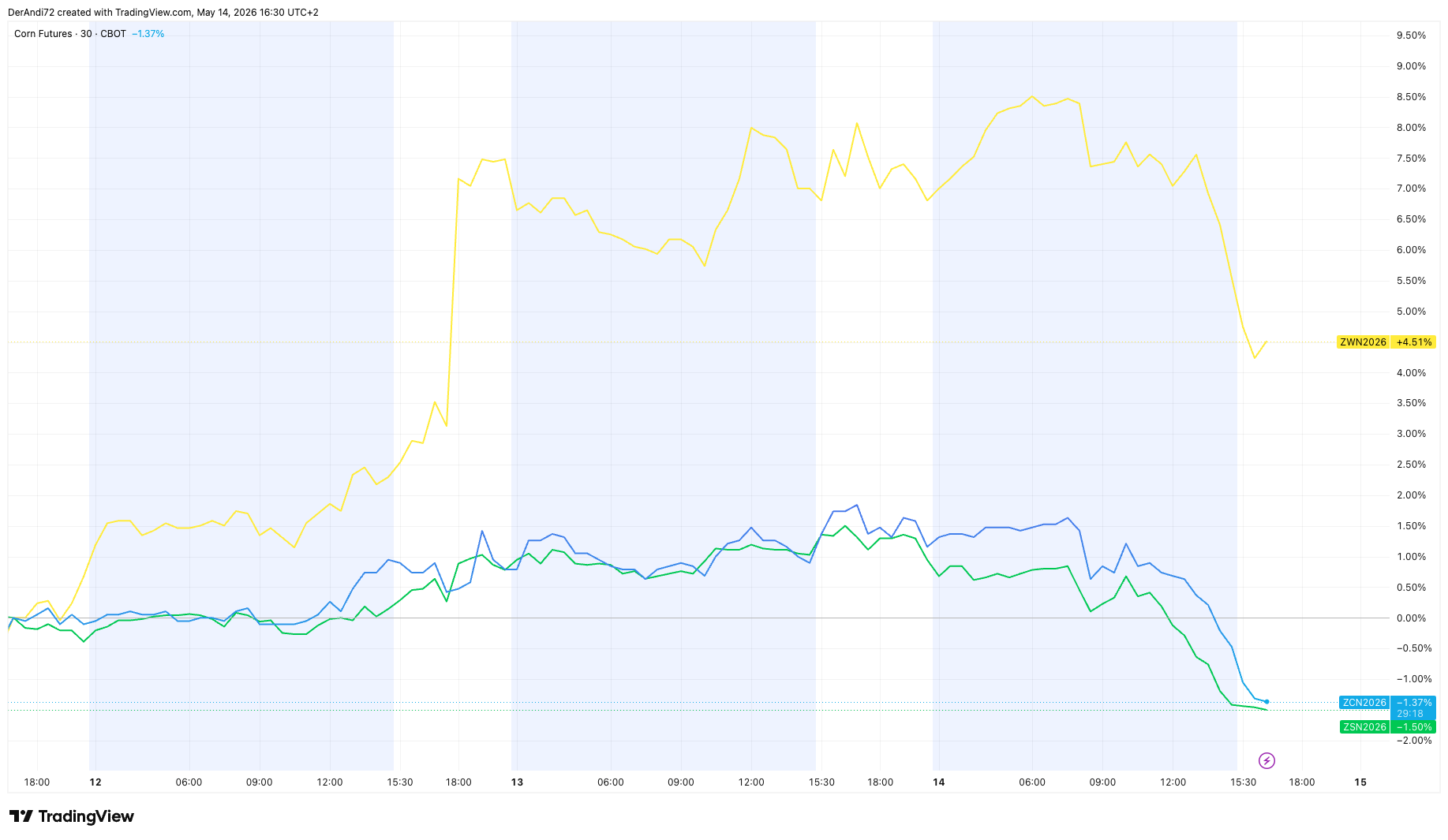

Wheat: the biggest reversal versus April

Wheat delivered the clearest bullish surprise in the May WASDE. In April, the market still looked heavy due to comfortable old-crop stocks. In May, however, the USDA introduced the first full 2026/27 outlook — and the new-crop picture changed dramatically.

U.S. wheat production is projected at 1.561 billion bushels, down sharply from 1.985 billion bushels in 2025/26. Ending stocks are projected at 762 million bushels, down from 935 million.

The main driver is winter wheat. The first survey-based forecast showed winter wheat production down 25% from last year, mainly due to sharply reduced Hard Red Winter output.

Globally, wheat production is projected at 819.1 million metric tons, down from last year’s record 843.8 million tons. Major exporters including the United States, EU, Argentina, and Australia all contribute to the decline.

From a trading perspective, wheat has now moved from “heavy but watchable” to one of the strongest weather-risk markets heading into summer.

Corn: not explosive yet, but structurally tighter

Corn was less dramatic than wheat, but still supportive. U.S. corn production is projected at 15.995 billion bushels, down from 17.021 billion in 2025/26.

U.S. ending stocks are projected to fall to 1.957 billion bushels, compared with 2.142 billion in 2025/26. The season-average farm price is projected at $4.40/bu, up from $4.15/bu.

The more important global point is that world corn ending stocks are projected at 277.5 million metric tons. If realized, this would be the lowest level since 2013/14.

Corn therefore remains a market where weather can quickly become the dominant driver. The WASDE alone is not a panic-bullish report, but it creates a tighter foundation before the key U.S. summer growing season.

Soybeans and soybean oil: biofuel demand takes over

The soybean complex was mixed on the surface, but very important underneath.

U.S. soybean production is projected at 4.435 billion bushels, up from 4.262 billion in 2025/26. However, crush demand is also projected to rise strongly to 2.750 billion bushels.

The real story is soybean oil. USDA projects soybean oil use for biofuel at 17.8 billion pounds, up from 14.2 billion pounds in 2025/26.

That is a major demand shift. The projected soybean oil price rises to 70 cents/lb, compared with 63 cents/lb in 2025/26.

For traders, this means the soybean complex may increasingly split into different stories:

- Soybean Oil: structurally bullish due to biofuel demand

- Soybean Meal: supported by higher crush

- Soybeans: more balanced due to larger production and South American competition

Sugar: quietly supportive

Sugar did not receive the same attention as wheat or soybean oil, but the report was still supportive.

U.S. sugar production for 2026/27 is projected at 8.810 million short tons, raw value, down from 9.239 million in 2025/26.

Beet sugar production is expected to decline, while Florida cane sugar production was affected by winter freeze damage. As a result, the U.S. stocks-to-use ratio is projected at 13.5%.

Sugar remains strongly influenced by Brazil, energy prices, ethanol parity, and currency movements, but the May WASDE itself leans constructive.

Cotton: mixed, but not the main story

Cotton was less exciting than wheat, corn, or soybean oil. U.S. production is projected at 13.30 million bales, slightly below the prior year, while ending stocks are projected at 3.90 million bales.

The global balance sheet does not show the same urgent tightness as wheat or vegetable oils. For now, cotton remains more dependent on macro sentiment, Chinese demand, weather, and broader risk appetite.

Trader takeaway

The May 2026 WASDE was much more bullish than April. The key change is that old-crop comfort has now been replaced by new-crop risk.

- Wheat: strongly bullish after a major production cut

- Corn: constructive, with weather risk now critical

- Soybeans: neutral to constructive

- Soybean Oil: very bullish due to biofuel demand

- Sugar: supportive due to tighter U.S. balance sheet

- Cotton: mixed and less compelling

For active traders, the most important markets after this report are wheat, soybean oil, and corn. Wheat is now the clearest bullish shift, soybean oil has the strongest structural demand story, and corn remains one weather event away from becoming a much more aggressive upside market.

Potential deep dives after this report

This WASDE opens the door for several focused follow-up articles and TradingView analyses:

1. Wheat Shock 2026

Compare March Prospective Plantings, May WASDE, winter wheat production, HRW weakness, COT positioning, and seasonal patterns.

2. Soybean Oil & Biofuel Demand

Analyze soybean oil demand, EPA renewable fuel policy, crude oil correlation, crush margins, and ZL price reaction.

3. Corn Weather Risk Map

Track U.S. Corn Belt weather, planting progress, stocks-to-use, seasonal tendencies, and possible spread trades.

4. Sugar Tightness & Energy Link

Review U.S. sugar supply, Florida freeze impact, Brazil cane mix, ethanol parity, and crude oil sensitivity.

Outlook into the next WASDE

The next WASDE reports will be especially important because May only gives us the first full 2026/27 framework. The market will now start testing these assumptions against real weather, planting progress, crop condition data, and export demand.

- Wheat: Watch whether further HRW downgrades appear and whether global exporters tighten further.

- Corn: Follow U.S. planting progress, early crop condition ratings, and any summer heat/drought risk.

- Soybean Oil: Monitor whether price action confirms the biofuel demand story or if the market had already priced it in.

- Soybeans: Watch export demand, crush pace, and South American competition.

- Sugar: Track Brazil, energy prices, and whether U.S. production cuts continue to tighten the balance sheet.

The key question for the June and July reports will be whether this May WASDE was only a first warning signal — or the beginning of a broader agricultural commodity repricing.